Table of Contents

The Common Narrative

“The Fed prints money” has become the default explanation for everything wrong with the economy. It’s also a convenient distraction that lets the real culprits off the hook.

The story we tell ourselves about money printing is a relic of the gold standard, when central banks literally minted coins or printed paper redeemable for gold.

Dual Mandate

Central banks are in fact very limited in their scope. Most are operating under a “dual mandate”, which consists of:

- Maximizing employment

- Stabilizing prices

Needless to say, those two goals are often in conflict, but everything a central bank does is scoped by its mandate.

It’s About Spending: COVID Monetarism vs QE

Monetarists always warned that increasing money supply leads to inflation, and it’s hard to dismiss them after what we saw during the COVID pandemic. Money supply surged in 2020, and by 2021 inflation followed. The correlation was clear, even if the causation was arguably more nuanced.

QE didn’t trigger inflation after 2008 because swapping bonds for reserves only fuels inflation if those reserves circulate, and they didn’t. Banks hoarded them, velocity collapsed, and inflation never arrived.

What Actually Happens

Central banks don’t fund deficits directly. The government issues bonds, dealers buy them, and the money gets spent.

That said, the central bank is obviously the biggest player in the government bond market. By keeping demand high and yields low, the Fed enables larger deficits than the market would otherwise tolerate, stimulating aggregate demand and contributing to inflation, much like old‑fashioned money printing.

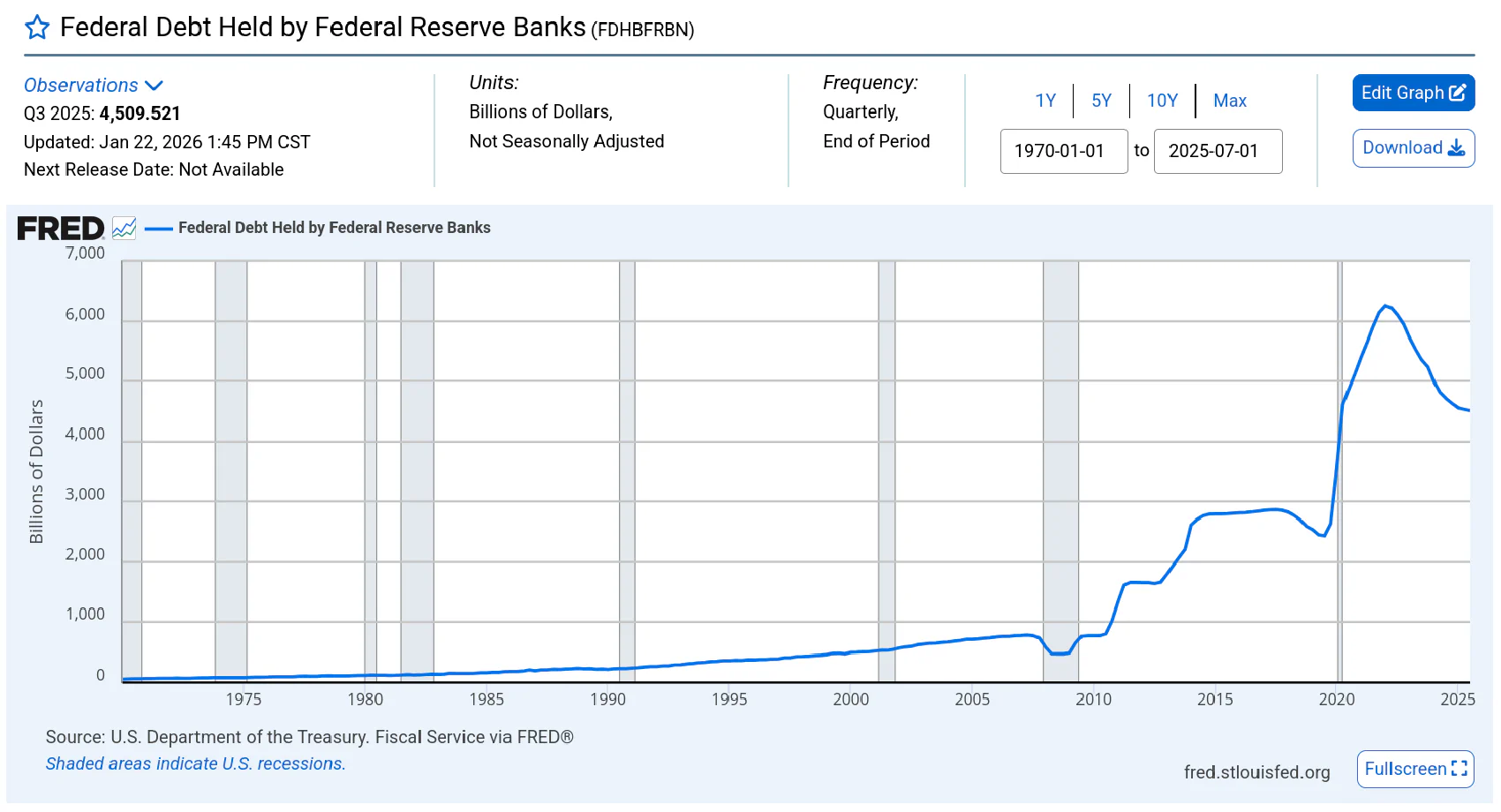

What if the Fed Sold All its Bonds?

The immediate effect would be a massive supply shock in the bond market. With demand unable to absorb that much supply without a major price adjustment, bond prices would plummet and yields would spike. Mortgage rates, corporate borrowing costs, and government debt service would all jump virtually overnight.

Of course, this is just a thought experiment since the Fed would never do this. Selling its entire portfolio would directly undermine its dual mandate.

Fed Needed QE More Than Banks

In 2008, banks weren’t lobbying for the Fed to buy their bonds. The Fed came to them, not the other way around. With interest rates already at zero, conventional tools were exhausted. QE was the only lever left when doing nothing was politically unacceptable.

Banks participated because the Fed offered to buy assets at favorable prices during a panic, but most large banks would have survived without it. The real beneficiary was the Fed itself, which needed QE to maintain the illusion of control when its traditional toolkit had run dry.

Helicopter Money

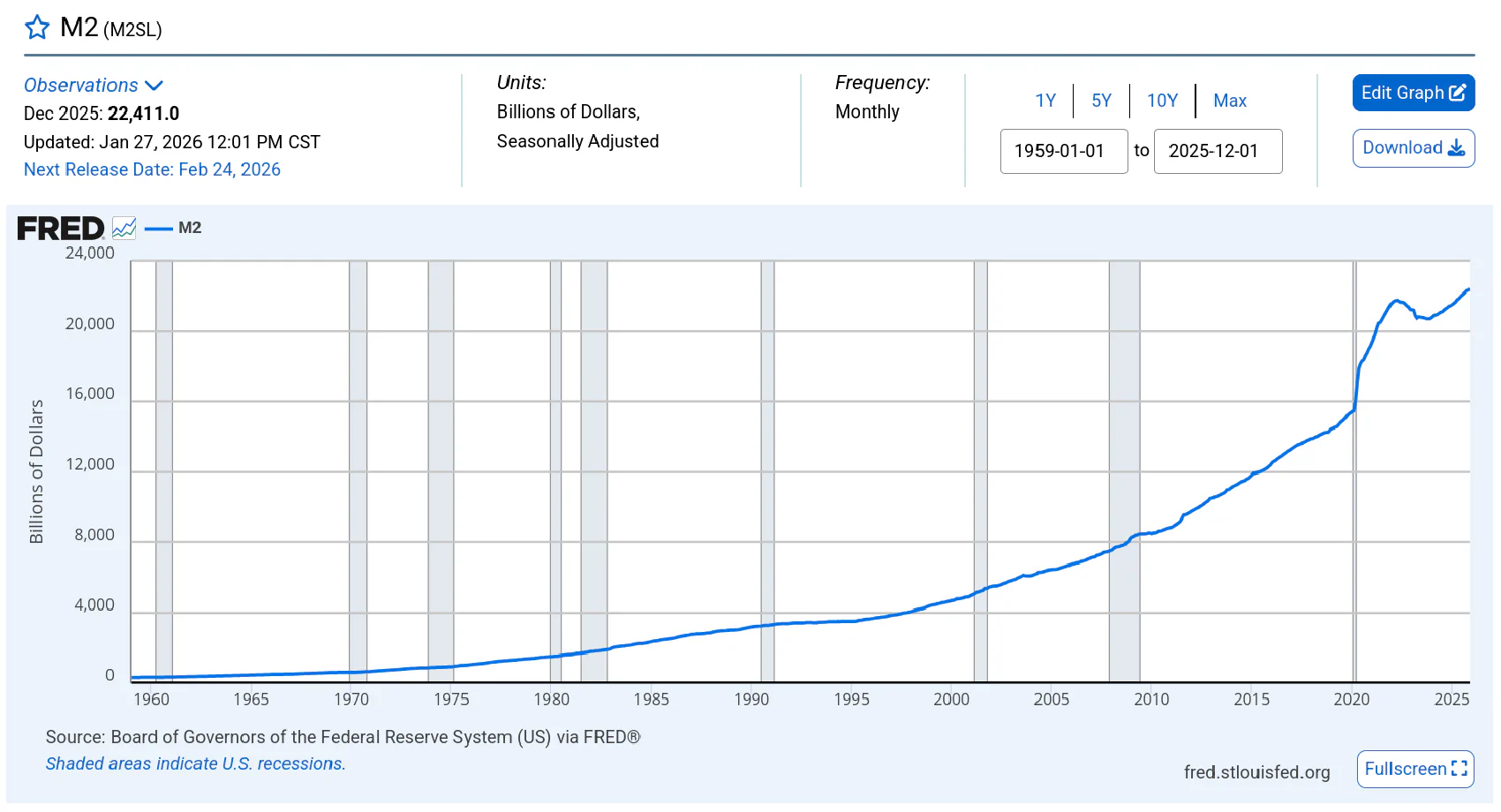

Critics call QE “printing money” because it expands the monetary base. That’s true for M0, but base money doesn’t automatically translate into new demand or inflation.

The central bank can flood the system with reserves, as it did after 2008. But broad money (M2), the measure that actually matters, is created primarily by private banks through lending.

In 2020, the Fed once again deployed QE, but this time the Treasury acted alongside it, sending checks directly to households through stimulus payments, expanded unemployment benefits, and PPP loans.

That money landed in checking accounts, and unlike banks, households spend. They buy groceries, pay rent, order from Amazon. Each transaction becomes someone else’s income, ready to be spent again. That circulation is what finally pulled inflation out of its long hibernation.

Who Really Prints the Money

The real problem is credit creation, and private banks do most of it.

When banks make loans, they create money. Your mortgage didn’t come from some pool of pre-existing savings. The bank created it, at the moment of lending, by typing numbers into your account. The money didn’t exist before you borrowed it.

The real “printing press” is the ledger system banks run. They’re the ones creating money out of thin air every time they approve a loan. The central bank enables it, yes. But the banks are the ones pulling the trigger.

The Sovereignty Question

When the money supply expands, it’s not just an economic act. It’s a political one. It transfers wealth from savers to borrowers via inflation. It distorts price signals. It rewards the connected and punishes the prudent.

The ability to create money is the ultimate form of power over others, and private banks are the true creators.

Conclusion

The Fed buys bonds to manage interest rates, provide liquidity, and stabilize markets. Swapping bonds for reserves changes nothing about a bank’s lending capacity.

The “printing” narrative is a distraction. It lets us blame a single institution for a system where both central banks and private banks are complicit.

Modern money is just a database. And like all databases, it’s controlled by whoever holds the keys. The Fed holds some, but it’s far from the only player.